Geithner: balancing the budget will

involve some difficult choices on the

part of lawmakers and

“will require sacrifice from all Americans.”

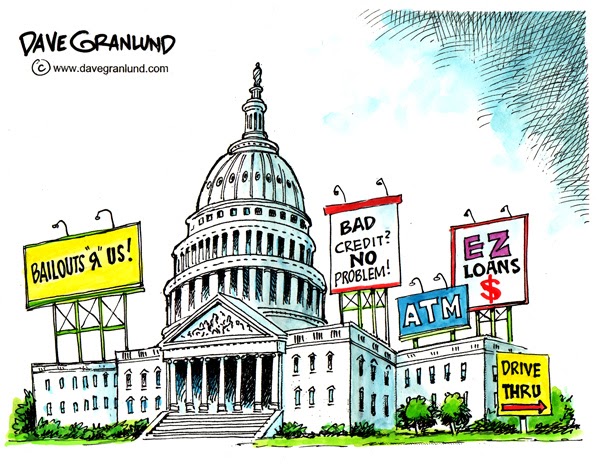

AIG BAILOUT

Automobile Tax Credits (Hybrid Gas-Electric)

BAB (Build America Bonds)

Big Oil Tax Subsidies Act (roughly $8 billion per year)

Cash For Caulkers

Cash For Clunkers

Chrysler BAILOUT

Consumer Energy Efficiency Creidts

Fannie BAILOUT

First Time Homebuyer Tax

Freddie BAILOUT

General Motors BAILOUT

HAFA (Home Affordable Foreclosure Alternatives a.k.a. "Exit Gracefully")

HAMP (Home Affordable Modifcation Program)

HARP (Home Afrfordable Refinance Program)

Home Energy Efficiency Improvement Tax Credit

HHF (Hardest Hit Housing Markets)

Operation Enduring Freedom (gov't speak for Afghanistan War)

Operation Iraqi Freedom (gov't speak for Iraq War)

PRA (Principal Reduction Alternative)

TARP (Troubled Asset Relief Program a.k.a. Too BIG to FAIL)

UP (Home Affordable Unemployment Program)

...and so on..and so on...

No, it's Not Colic

ABC News

By Arlette Saenz

2/15/2011

ABC News’ Arlette Saenz reports: In a hearing before the House Ways and Means Committee, Treasury Secretary Timothy Geithner defended the president’s budget proposal as a means of restoring fiscal responsibility to an economy riddled by a mounting national deficit.

“Our deficits are too high. They are unsustainable, and left unaddressed, these deficits will hurt economic growth and make us weaker as a nation,” Geithner said. “We have to restore fiscal responsibility and go back to living within our means.”

Geithner targeted entitlement programs as the key to reducing the national debt while insisting that Social Security benefits remain protected.

“Our long term deficits that we face over the next century are primarily driven by rapid rates of growth in healthcare costs and to a lesser extent by Social Security obligations. The most important thing we can do to reduce those long term costs is to reduce the rate of growth in healthcare costs.”

But committee members pounced on the president’s budget proposal for not providing enough guidance in curbing entitlement programs.

“Americans shouldn’t have to wait any longer for some real solutions, and frankly, this budget is a missed opportunity,” Chairman Dave Camp, R-MI, said. “There‘s nothing on entitlement reform, and there’s little more than lip service about getting the deficit under control.”

“For so many of us, we are just dumbfounded, astounded by the fact that the administration hasn’t taken this opportunity to address the issue of entitlements,” Rep. Tom Price, R-GA, said. “There’s no evidence of this administration taking the lead and initiative on entitlement reform. You’ve taken the lead and initiative in expanding entitlements and expanding automatic spending.”

Geithner acknowledged that balancing the budget will involve some difficult choices on the part of lawmakers and “will require sacrifice from all Americans.”

Geithner took a brief moment to tout the success of TARP, which was initially projected to cost taxpayers $350 billion but is anticipated to show a positive return for taxpayers.

“I think it will prove to be the most successful financial rescue in modern history,” Geithner said. “Even recognizing, we face a lot of challenges ahead in digging out of this crisis, repairing the damage caused by it.”